🚕 Uber & Lyft and the road to profitability

A tale of two companies

This newsletter offers deep takes on the intersections between mobility and technology. You can subscribe here:

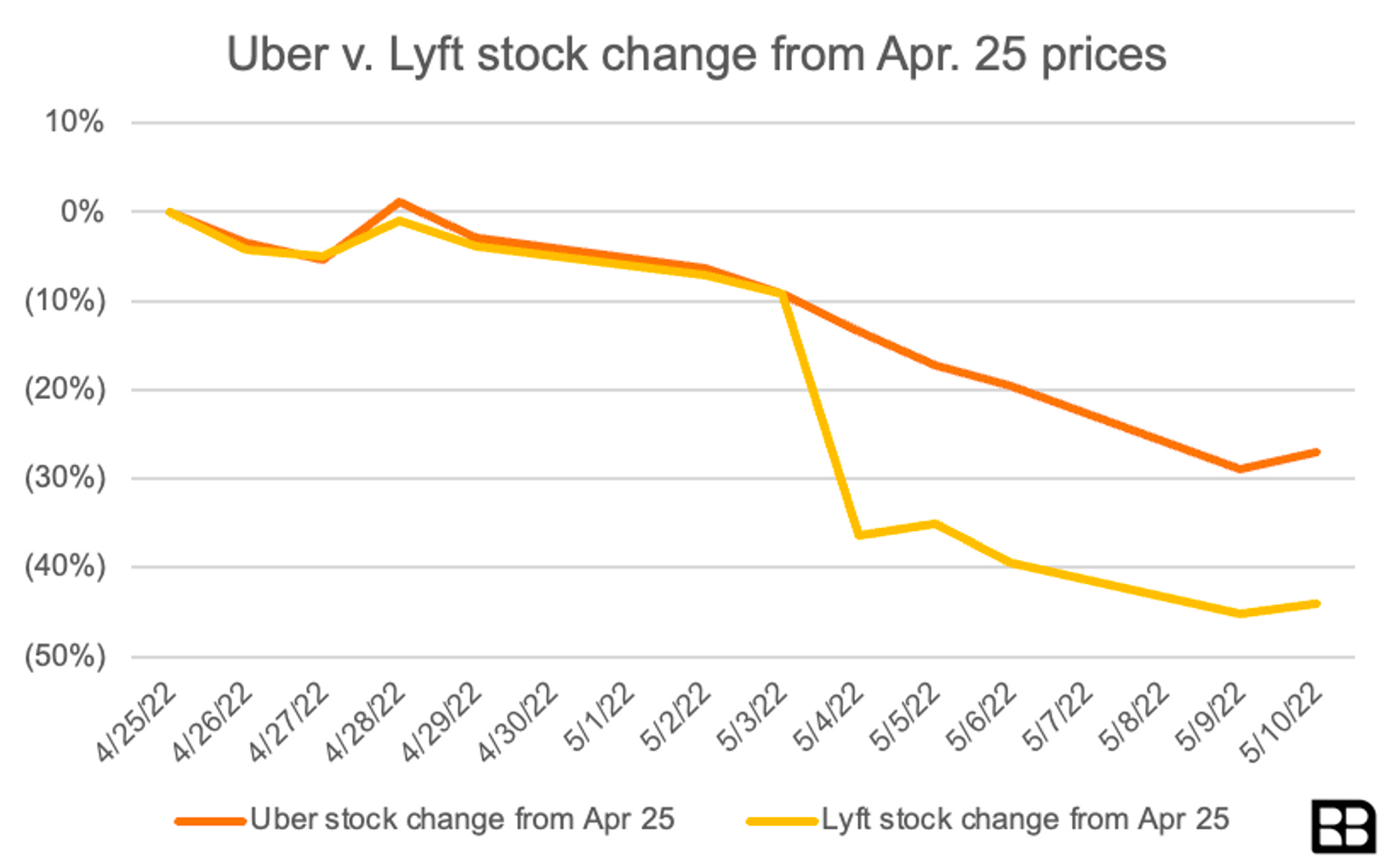

Lyft’s Q1 earnings this month tanked the stock 30% in the hours after the call. The concern became contagion, dragging Uber down even before Uber’s earnings were announced. Dipping 10%, Dara rushed news to market as if to say “hold on - we’re not Lyft!” and made the rare decision to move up earnings by a day.

It worked - while Lyft remained in the gutter, Uber turned its decline around and finished off down only a few percentage points from the days prior.But why? Lyft reported a nearly $200M loss, and Uber reported a nearly $6B loss. Isn’t that worse? It certainly fed Uber naysayers

.

But why? Lyft reported a nearly $200M loss, and Uber reported a nearly $6B loss. Isn’t that worse? It certainly fed Uber naysayers.

But that $6B loss masks the real story. Let’s separate operational profit (which many tech companies call “adjusted EBITDA”) versus true profitability (generating free cash flow).

Actually, Uber is already sort of profitable

Operational profit is a question of “can Uber make more money than it spends on rides, food delivery & freight?” By successfully hitting positive adjusted EBITDA semi-regularly, Uber is now showing that this is in fact the case, and it’s how they claim “operational profitability.”

Q1 was a show of great strength for Uber’s core businesses. Food and grocery delivery kept drivers earning throughout the pandemic, priming Uber for the surge in riders we’re seeing today. CEO Dara calls this the “power of the platform.” Drivers are plentiful and getting a lot of gigs on Uber, giving Uber the breathing room to cut back on bonuses and incentives, yielding operational profitability. It is beginning to seem like Uber’s scale flywheel is spinning without help.

Understanding the $6B net income loss

On top of that operational business though, you have a lot of other heavy areas of spend. Uber previously invested a lot of resources into new market expansion (yielding a major ownership chunk of China’s Didi) and introducing new products (yielding a major chunk of autonomy leader Aurora). Recently, DiDi was slammed by China’s tech crackdown, and Aurora stock is down as well. Almost 95% of Uber’s Q1 “losses” were simply writedowns of these holdings. Those aren’t cash losses today, nor do they threaten the viability of Uber’s (increasingly profitable) operating businesses.

Back to Lyft

As Lyft didn’t have a delivery offering, its driver base shrunk a lot during COVID. Lyft had to spend heavily on incentives to get them back - and signaled it will probably need to continue doing so. That’s a big problem that triggered the stock selloff. Lyft’s marketplace flywheel is in need of more nudging. And while Uber’s mega projects (China, autonomy, flying cars) might be falling apart, its core business is a flywheel that’s ... flying (and remember that Uber’s ridehail business is much bigger AND growing top-line much faster than Lyft’s). Lyft’s picture isn’t great.

As much as it would seem that these marketplaces are commoditized for drivers and riders, Harry the Rideshare Guy told me recently that in LA Uber drivers are averaging over $30/hr, with top drivers hitting $60/hr. In contrast, Lyft drivers have lower density meaning the network has long ETAs and a lot of cancellations, making things worse for both drivers and riders.

Newspeak

OK: Operational profitability isn’t real profitability though. Ridehailing company accounting is complicated (see this for a taste) and companies have long leaned on accounting and linguistic ambiguity to mask their losses to investors. When markets were kinder, they could get away with it. But in the height of the current tempest, Dara sent an urgent email to all employees.

Breaking rank with most tech CEOs, Dara didn't wax poetic about Uber's transformative vision. He cut straight to what most big tech CEOs ignore: what investors demand. And the message was clear - not just growth, operational breakeven, "adjusted EBITDA" profitability...

The message: Uber is going to generate free cash flows.

Dara’s forecasts are finally clear: $300M in FCF this year, and $1.8B in 2023. If Q4 looks the way they are (finally) guiding, Uber won’t just be the company famous for buying growth. It will also be the first company to take ridehailing into the next stage of its life: sustainability.

This article was first published in the RedBlue Newsletter on May 19, 2022.